01

The delivery cash cow

Saudi first.

GCC and beyond later.

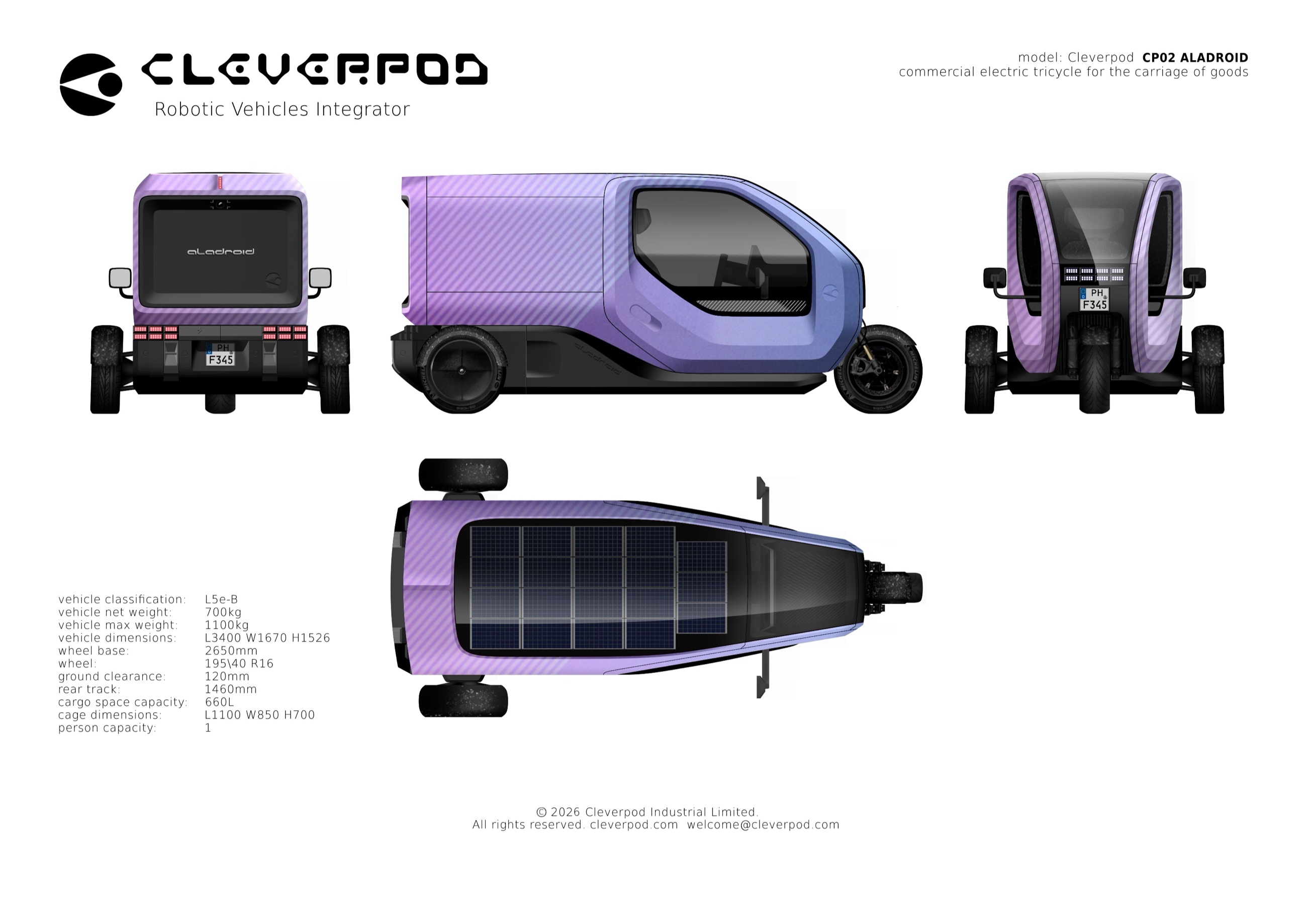

- One product (CP02 delivery vehicle), one business model: a monthly subscription per vehicle bundling the vehicle, operator training, fleet software, insurance, compliance, and a defined uptime SLA.

- Saudi ramp: Riyadh, Jeddah, and Dammam first; other Saudi cities to follow.

- GCC and beyond: additional upside on the same engine, not assumed in the headline returns.

- The financial model exclusively reflects the Saudi delivery fleet business, end-to-end.