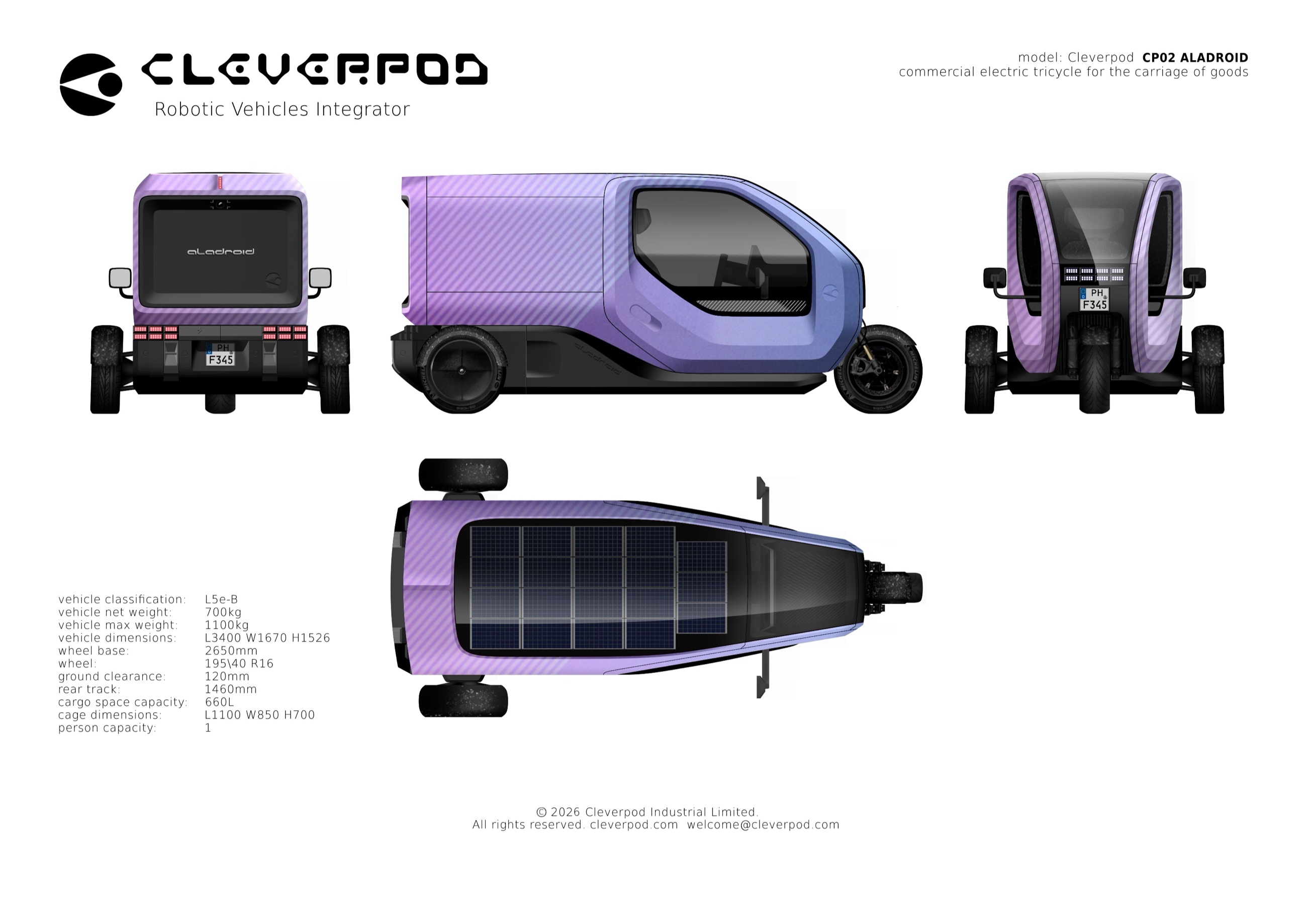

Non-app delivery — additional upside Not in the model

Everything above is sized only against orders that flow through delivery apps. A large share of Saudi last-mile delivery never touches an app — restaurants and retailers running their own delivery, pharmacy and grocery direct-to-door, parcel and courier, and B2B distribution. Cleverpod sells the vehicle, which is indifferent to whether the order came from an app, so this is additional addressable fleet on top of the 8.2% / 1.8% above. For scale, Mordor separately sizes Saudi's formal courier/parcel (CEP) market at ~SAR 7.5 bn and its last-mile delivery market at ~SAR 4.7 bn by 2031 — but these measure logistics-service revenue, not app spend, so they are shown only as directional context and are not added to the headline shares. It is deliberately excluded from the model: pure upside.